Welcome one and all to the 100th episode of the Investopedia Express. We are so grateful to all of you for listening and to all of our guests who’ve climbed aboard the Express to make us smarter every single week. Now let’s get down to business, and we got a wake up call to end the week, and that has reset the tone for the rest of the year.

Words from Fed Chair Jay Powell high up in the Teton Mountains near Jackson Hole, Wyoming, blew an icy chill over the equity markets last Friday. The Dow Jones Industrial Average fell 3%, with losses accelerating into the close. You hate to see that. The S&P 500 fell 3.3% and the NASDAQ fell nearly 4%. For the S&P, Friday’s 3.4% drop was the seventh daily decline of 3% or more this year, according to Charlie Biello. There’s only been three other years with that many or more 3% drops: 2008, 2009, and 2020. Friday’s losses capped two straight weeks of declines, as the S&P has now given up 5.2%—its worst stretch since mid-June. Investors who’ve been banking on the Federal Reserve to pivot to a less hawkish stance may have misplaced their optimism, and many have likely realized that as investors have switched their flow show lately. According to data from Refinitiv Lipper, $1.2 billion was pulled out of U.S. stock funds last week after a brief stretch of inflows in the first half of August. Since the beginning of June, however, investors have pulled more than $44 billion out of the U.S. stock market, which is kind of amazing when you consider that the S&P 500 rallied more than 10% off its lows since mid-June.

There’s a lot of money on the sidelines, and there are an increasing number of investors and traders who are now actively betting against the stock market and playing the pain trade. According to data from the Commodity Futures Trading Commission (CFTC), there are more than 260,000 futures contracts that are short the S&P 500. That’s a big bet that they think it has further to fall. Most of those positions, according to the CFTC, are held by big hedge funds. Either the masters of the universe are right this time, or they are about to awaken the retail trading army that has been asleep since May 2021 and draw them back into the market to put the squeeze on the shorts. Something tells me, though, that with the fears of a recession and no more government handouts (except that student loan relief), that’s not so likely to happen.

The Fed still has a lot of work to do to bring inflation back down to its 2% target range. It’s going to take a while. According to Strategas Asset Management, when we look at the past eight rate hike cycles here in the U.S., the Fed continued to raise rates until the Fed funds rate, which is what we call the prime rate, is greater than the Consumer Price Index (CPI). The Fed funds rate right now currently sits at 2.5%. CPI, or inflation, is at 8.5%. We’ve got a long way to go, my friends. Higher for longer, which may trigger a recession.

And while everyone is debating whether or not we’re in a recession, let’s get back to the fundamentals on that question. The NBER, the National Bureau of Economic Research, which identifies recessions once they’ve passed, looks at six indicators to determine whether it is or isn’t or was or wasn’t. What are those indicators? Real personal income; real personal consumption expenditures (that’s the PCE index we keep talking about); industrial production; employment, or nonfarm payrolls; the employment level, otherwise known as the unemployment rate; and real manufacturing. Five of those six indicators are still positive year to date, believe it or not. Industrial production and employment have been particularly strong lately. Manufacturing? Not so much, likely because of inflation at the producer level. Looking at the economy the way the NBER looks at it. This is no recession, at least not yet.

What’s in This Episode?

Subscribe Now: Apple Podcasts / Spotify / Google Podcasts / PlayerFM

It’s our 100th episode, so light the candles and ring the bells. We are throwing a little party on the show today, so I brought two of our all-stars back on to the Express to celebrate with me. You know them well if you know the show or if you hang out in Fintwit like some of us. On the mound, the one-and-only JC Parets of AllStarCharts, the chart master, the sommelier, and a good friend of Investopedia. And at the plate from Boston’s Back Bay, batting from the right side, a frying pan in one hand and the stock market in the other, the master chef, the broker’s broker, Kenny Polcari, also a good friend of Investopedia. Thank you both for being here on our 100th.

JC:

“That was that was really good. Did you write that yourself?”

Kenny:

“That was very good. I’m so impressed. I love the way you did that.”

Caleb:

“I wrote that while you guys were talking about Florida a couple of minutes ago. I get a lot of inspiration from both of you. I follow you not just as an investor, but as a gastronomist. So, as a gift to the show, you guys are going to drop off a recipe and a wine pairing at the end of our convo because you’re experts in that. But first, Kenny, let’s talk about you. You approach things from the macro perspective. I know you use some technical analysis, but you’re a big picture guy, right? You’re looking at the big picture in the U.S. stock market today. Was mid-June the bottom or just a bear market rally, a bull trap, or whatever we want to call it out west.”

Kenny:

“So, I do think that June was the bottom. Now, unless the whole world starts to fall apart in the next month and a half, I do think that the June 16 low was the bottom. Thirty-six, 25ish, something like that. I think that we could test lower from here, but I do think the low’s in. Now look, if we suddenly get CPI… which I actually think is not going to continue to roll over. I think CPI is going to level off and then actually lift its head again. And then, depending on how the Fed reacts, could see us in fact break that. I don’t think that’s going to happen. I think the Fed is going to remain aggressive, but I don’t think the CPI is going to turn up so much that it’s going to cause the Fed to start to get really nuts in terms of their rate increases.”

“So, while I like the market here, I’m a little bit cautious going into September. September tends to be kind of a volatile, anxious time in the markets. September is the worst month, we know that. They lose about almost 2% on average by the end of the month. That, coupled with where we are now in terms of CPI, the Fed, Jackson Hole. Now the out of control spending in the government is going to, I think, provide some additional headwinds for stocks in the markets in September. While I’m a long-term bullish, I always am, I’m just a little bit cautious going into September and building up a cash position to put to work when I think that that the worst is over for September.”

Caleb:

“Good big picture stuff. JC, from the technical perspective, does any of that matter, or are the charts telling us a wholly different story?”

JC:

“Well, let’s be clear, all of the things that Kenny say, of course, matter. Those are things that money managers around the world take into consideration when they’re making their investment decisions. We as technicians just don’t need to care about what the reasons why investors are doing what they’re doing are. So, we rather just follow the footprints. I don’t so much care why they’re doing it. I want to know what they’re doing.”

“And what we’re seeing is actual buying. We saw one of the biggest short squeezes on record in the history of the stock market off of the June lows. The New York Stock Exchange, new 52-week low list peaked in mid-June. That was over two months ago. The average stock on the Nasdaq’s up over 40% off those lows. The average stock on the New York Stock Exchange is up over 30% off of those lows. And you’re seeing sector rotation. In other words, the areas that were struggling are now picking up the slack and catching up with the leaders. We’re seeing that. You know what we’re not seeing? We’re not seeing new lows. We’re not seeing oversold conditions. We’re seeing overbought conditions. We’re seeing new highs expanding. Those are characteristics of uptrends, not downtrends.”

Kenny:

“No, no. And I agree, JC. I think all that’s great. But look, we’re seeing that move off the bottom. We’re seeing the 18% move off a market that got into a well-oversold position in June. In my opinion, I thought it was overdone. So, therefore, I wasn’t really surprised to see the snapback rally. I was surprised it maybe went on a little bit longer than I thought or was a little bit more aggressive than I thought, considering what I think is coming next. But to your point, it also made sense that a lot of the laggards, the ones that have gotten beaten up the most, were certainly the ones that people jumped into. But they’re also going to be the ones that they throw out the window the minute the **** hits the fan.”

Caleb:

“JC, you noted in your note—I think it was this week—that it’s consumer discretionary, tech, industrials, these are the sectors that have been rallying. So, what does that tell you, Kenny, from investor appetite? And then, JC, from a trend perspective.”

JC:

“Yeah, no question. Technology, one of the leaders, consumer discretionary… really reinforcing the fact that the growth stocks that got beat up the most are the ones that bounce the most, which is what Kenny was just saying. And by the way, you can argue industrials are actually the most important sector in America. It’s got the highest correlation of all of the S&P sectors with the overall market. But I’ll point you to utilities because a lot of the permabears and the angry people out there keep talking about the strength in utilities, how it’s hard to get excited about a stock market where utilities are leading. Let me tell you something, my friends, from 2004 to 2007, the stock market did fantastic, and utilities led the whole way. In fact, utilities doubled the performance of the S&P 500 during that period. And that was one of the greatest periods of all time. It was early in my career. I remember it well. Utilities were a leader. They’re a leader today. That’s perfectly normal.”

Kenny:

“Right, and utilities are leading. You can argue that utilities are leading because of their steady… you look at a lot of investors. There are a lot of older investors that use utilities as a source of income, dividend payers. They’re safe, they’re stable, they provide stability to their portfolios. And those are the ones that have a lot of the money right now. So, it makes perfect sense. And I like utilities. Now, I own them, they are part of my portfolio, but I’m also 60. I’m in that position where I have to be looking to protect my portfolio more than take outsized risk on my portfolio.”

Caleb:

“Last time we talked, JC, you argued that we were in the early stages of a commodity supercycle, and those play out for years. Those don’t take a couple of months. Those play out over a long period of time. But prices have come way off for a lot of them. Are they taking a breather here as we potentially head into a global recession? How do you see the commodity supercycle now?”

JC:

“Well, I still think we’re in the early stages of that. And let’s remember, we got a pullback, but we also got one of the most historic rallies in a lot of these commodities in history prior to that pullback. So, you have to put things in perspective. I like energy here. We’ve been buying energy. The pullback in energy, I think, was one to buy. Warren Buffett’s all over it. He keeps buying Chevron. Dude’s filing with Occidental Petroleum like every day. The more Warren Buffett’s buying, I’m buying too. I’m not buying cause Warren Buffett’s buying. But the fact that I’ve been buying and so is he, I’m not mad about it.”

Caleb:

“Not bad company.”

JC:

“I’m not mad about it. But I do like the commodities. I do like energy. And particularly, if oil is above $88, I like energy. If it’s above $93, I like energy even more. And on the energy stocks themselves, XLE around $79 or $80, as long as XLE’s above those levels—those are the former highs from the past decade—all systems go, baby, let’s go.”

Caleb:

“The dollar may be the wizard behind the curtain in all of this. Strong greenback has been bad news for stocks all year, you guys both pointed out in your notes. Is that going to be the case for the rest of the year here as we potentially head into a global recession, global slowdown. What do you think?”

Kenny:

“I think it has to be because the dollar is going to respond to every time the Fed starts raising rates against… because higher rates are going to attract capital into the market, the dollar is going to benefit. So, I expect that they’re going to raise rates at 75 basis points in September. I don’t know. Everyone seems to convince themselves, or a lot of people seem to convince themselves, that the Fed’s going to pivot and go soft to go 50 basis points. I don’t think so. I just don’t see it. Inflation’s at 8.5%. And you may say, ‘Oh, well, it ticked down two-tenths of a percent last week.’ That’s great, but wait till they start putting oil back into the equation as it’s making its way higher and probably going out $120 before it goes to $60. In any event, CPI is going to light up again and that’s going to force the Fed to remain, if not as vigilant, even more vigilant. And that’s going to send the dollar higher. And that will put pressure on commodities, by the way. I mean, it won’t put pressure on oil so much, but it might put pressure on some of the other commodities. Lumber, might put pressure on food commodities, because they’re priced in dollars.”

Caleb:

“JC, what are the charts telling you about the dollar’s strength?”

JC:

“Well, the dollar’s strength didn’t put any pressure on any of those commodities in the first half of this year. So, I don’t see why it might start doing that now. I would not overthink the inner market analysis there and more of like a ‘trade what’s in front of you’ situation because the commodities have been ignoring the dollar. As stock investors, as investors, as just humans in this world, I think it’s important to recognize that we’ve had a very, very, very strong negative correlation between the United States dollar and stocks and crypto. When the dollar peaked in late 2016 and started to fall, that was after the Trump election, stocks and crypto absolutely were up. 2017 was one of the greatest years ever. And then what happened in 2018? At the beginning of 2018, the dollar bottomed and started to rally and that put pressure on both stocks and crypto for quite some time. And then in March of 2020, the dollar peaked and started to fall. And what happened to stocks after March of 2020? Went on to have the greatest 52-week period in history. And then a funny thing happened…”

Kenny:

“Yeah, but…”

JC:

“Hold on, hold on. And then last spring, the dollar stopped going down and started to rally. And what happened? Stocks stopped going up and started going down. So, in my opinion, you can say that that’s just a coincidence, which is fine, you’re entitled to do that. You can say, ‘Okay, the correlation was negative and now moving forward, that correlation is going to change.’ You can say that, or you can make the bet that we’re making that the correlation is going to remain in place, and if you are bullish stocks or crypto, it’s not a ‘want’ a weaker dollar, it’s a ‘need’ a weaker dollar.”

Kenny:

“Okay, but listen, everything you say I agree with, that’s fine. But in March of 2020, as it was even leading up to March in 2020, interest rates have been zero for more than a decade. Where else was money going to go other than into stocks? It was crazy. They kept rates at zero, and then they printed all kinds of money, and then the Fed government started spending all kinds of money. And so, therefore, where were people going to go? They were forced into the stock trade, they had to be. What else were they going to get…?”

Caleb:

“Getting hot in this kitchen. And we haven’t even started with the recipes. But you’re right, there was a lot of government money coming at us. We had zero interest rates. Let’s talk about quantitative tightening. It starts this week. Big deal, little deal, or no deal? The Fed’s going to start selling off its balance sheet here. Kenny, what do you think?”

Kenny:

“Didn’t they already start doing $45 billion a month back starting in May or do they not really doing that? Were they not doing it, or were they supposed to be doing it? I don’t think they were doing it to the pace they set. Now suddenly they’re going to ramp it up to $90 billion a month starting in September. I’m curious to see if they really do that, because if they do that and they are aggressive in raising rates, then I think you have to watch out because then the bottom starts to fall out because the market, I don’t think, is expecting that they’re going to do both. They know that they’re supposed to reduce the balance sheet. I don’t think they’ve done it to the extent that they said they were going to do it starting in May. But I think they’re going to focus more on the rate side. They’re going to push rates up, and they’re going to go less probably than the $90 billion. I don’t think they’re going to reduce the balance sheet by $90 billion every month now going forward. I just don’t see how they’re going to do it and continue to be that aggressive on rates.”

Caleb:

“JC, what about all that supply coming on to the market?”

JC:

“I mean, I’m not really interested in what the Fed’s doing. I’m more interested in what the bond market and what the interest rates are doing, and that leads what the Fed is going to do. The Fed just does whatever the market tells it to do. The market tends to be a leading indicator. So, if we’re going to talk about where rates are heading, I would look at inflation-protected treasuries versus nominal yielding treasuries, and those have started to perk up with energy coming back. If you’re interested in what the Fed’s going to do, I would look at that. And if you have any interest at all in what the Fed’s going to do, I can’t imagine why. Like I said, if we’re having a stock market conversation, for me, I’m less interested in what the Fed is going to do. But if you really want to know, just look at the Fed funds futures, and they’ll just tell you. People are always guessing and going back and forth about what the Fed’s going to do—literally there’s a market for that. You can actually just go see what the bond market is pricing in.”

“I don’t necessarily know that what the Fed is going to do or not do is going to impact the dollar or the stock market. All I’m telling you is that the correlation, the strong negative correlation between stock market and crypto and the United States dollar is off the charts. Fed or no Fed, lower interest rates, higher interest rates… There’s no historically reliable correlation between interest rates in the United States dollar. I know you can compare it to what’s going on in Japan and blah, blah, blah. We can do it, and we play that game all we want. But the bottom line is, regardless of what the reasons are, the negative correlation is there. So, if you are betting on a rising stock market into the end of the year, or if you are betting on rising crypto prices into the end of the year, a weak dollar is not a want it is an absolute need.”

Caleb:

“Let’s get to some of our favorite indicators here, Kenny. I know, big macro guy. You look at a lot of things, but what is your favorite indicator of the moment that’s just giving you the clearest picture of how the market is going to play out over the next few months? What are you watching?”

Kenny:

“While you’re right, I do look at a lot of them, but the ones that I’m really focused on are the inflationary ones. So, it’s the PCE tomorrow. It’s going to be the CPI and PPI on the 13th and 14th of September. Right now, while I look at everything else (and the PMIs), services is now well into contractionary territory. It came in at 44.1. We’re a 75% services economy. That’s a key number to watch. Manufacturing, while it’s still in expansionary territory, the trend is down. That came in at 51.2. Fifty’s the dividing line, you know that. That’s been a downtrend. Between the inflation reports, the PCE, the CPI, and the PPI, I look at the PMI reports as well because those those indicators right now are giving me a sense of where the economy is and where the economy’s going and then the role that the Fed’s going to have to take.”

JC:

“JC, you look at thousands of charts every week. Hard to pick one, but what’s the one that’s got you excited at the moment?”

JC:

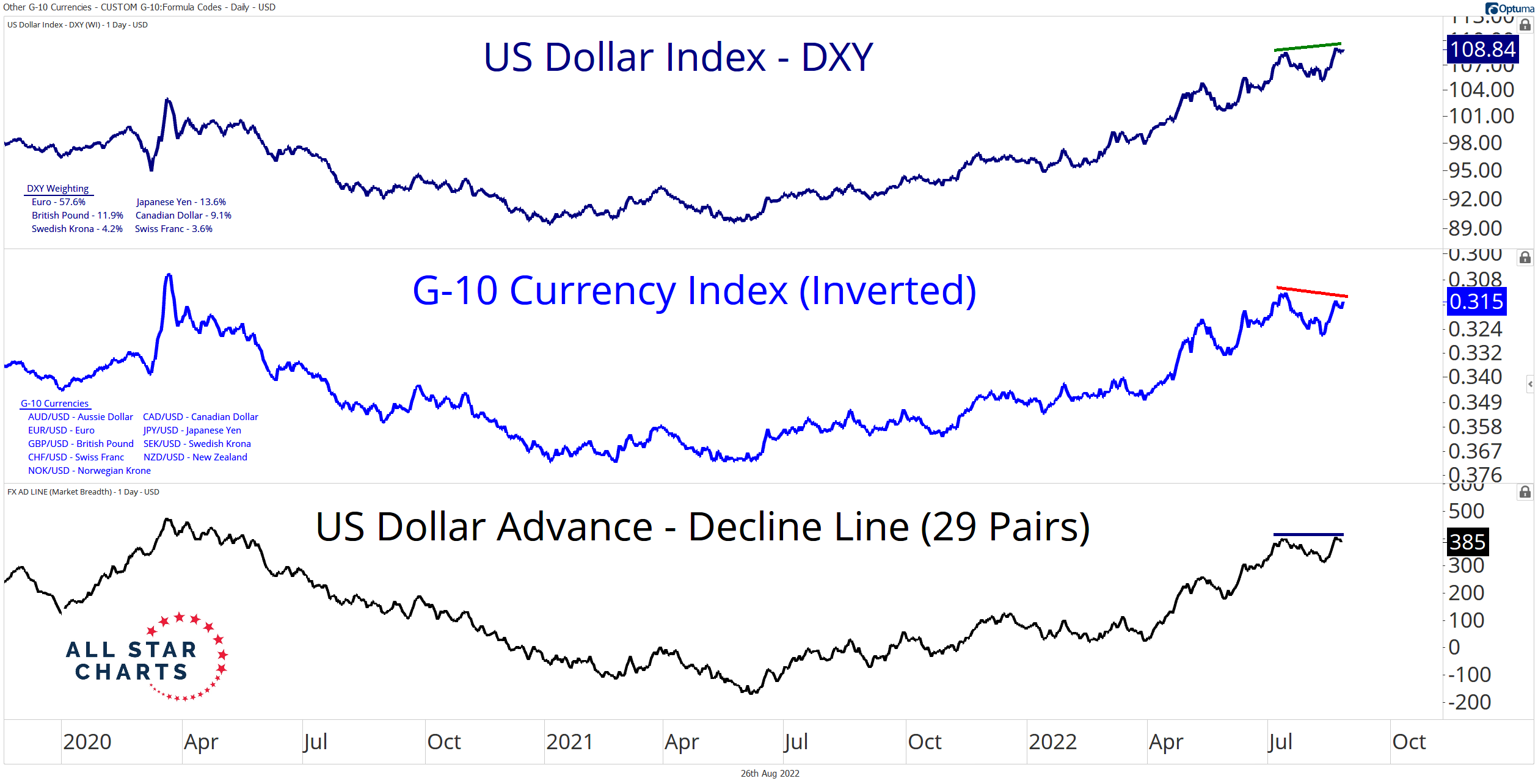

“Well, it’s definitely not any of those PMI or CPI; I could barely spell CPI. I’ll call Kenny and ask him. We got some guys on our team that keep me posted and all that stuff because they can’t help themselves. But for me, again, not to be Mr. Macro here, but it comes back to the dollar. So, here’s what I’ll point out. If you look at the euro and you look at the British pound retesting the summer lows… Literally as we’re recording this on Thursday, August the 25th, I believe, in the afternoon, euro and British pounds literally retesting the lows. What you’re not seeing is a retest in the lows in yen or AUD or CAD or emerging market currencies. You’re seeing really potentially positive divergence in all of those other currencies, while the worst ones out there, euro and British pounds in particular are retesting the lows.”

“What’s on my mind? I posted it recently, you can put it in the show notes if you’d like. An overlay chart of Great British pounds versus the United States dollar and the euro versus the United States dollar. And you’ll see them doing the exact same thing, retesting the summer lows. If those things break and those things collapse, the stock market’s going to be in a lot of pressure this September and October. And all of those bearish implications about the month of September are most likely to come into play. I think, if you’re bullish equities and you are putting money to work, you really need to see the euro and British pounds dig in, hold these lows, and just stop going down, and I think that would be a positive for stocks.

{kind=link}

Caleb:

“Great indicator. We’re going to put that in the show notes. And also, you can follow JC’s insights on Chart Advisor, the Investopedia newsletter all about technical analysis. But great insight from both of you. So, let’s head to the kitchen. I’ve been waiting for this the entire time as you guys were were talking through those markets. Kenny, what are we cooking right now? It’s the season. What do you got going on in the kitchen? And JC, I want you to follow with the wine pairing we’re having today.”

Kenny:

“So, listen, I gave this a lot of thought. I didn’t know if we should do something on the grill or something in the stove, something in the oven. And I chose going into the oven because summer’s over. Let’s get back into the kitchen. I’m thinking that we should have a delicious pork caprichosa cutlet. You want it on the bone? I want it absolutely on the bone. You want to buy the pork cutlet probably about an inch and a half thick on the bone. You want to season it, pound it out a little bit to soften it, season it with salt and pepper, dredge in flour, dip it an egg, and then cover it with seasoned Italian breadcrumbs, sear it on the stove in a saute pan with some butter just to brown the breadcrumbs. Put it in a baking dish, then go back to your saute pan. Add a little bit more butter, some white wine, warm it up, let some of the wine disappear, and then pour it over the chops. Cover them really tight with tinfoil. Bake them in the oven at 325 for probably an hour and a half, two hours long. You bake them in the sauce they get anyway. Pull them out, and then you’re going to serve them on a platter with arugula, cherry tomatoes, red onions, and Grana Padano cheese. You’re gonna mix that in a bowl and put that right on top of the chop when you serve it. It is delicious.”

Caleb:

“Oh my gosh. My salivary glands are so swollen, I can barely speak right now. JC, did you hear that? What are we going to open up and drink with that dish?”

JC:

“I’m going to go shopping for a house near Kenney’s house so I can start hanging out. Kenny, wow, that was amazing.”

Kenny:

“That’s such a great dish. That’s a really great dish”

Caleb:

“Whose car we taking?”

JC:

“Dude, let’s go. I walk out now.”

Kenny:

“You know what? That’s a really good meal.”

Caleb:

“What are we drinking, JC?”

JC:

“‘What are we drinking with that?’ That’s a great question because we got the pork and then there’s no carb. It’s an arugula salad, you said?”

Kenny:

“Yeah, it’s an arugula salad with cherry tomatoes and you got red onions and Grana Padano…”

JC:

“I think because you’re going cherry tomatoes, you want a high acid wine. So, I think you’ve got to go Sangiovese or Nebbiolo. I mean, you can go either. Maybe like a Barbaresco, but I don’t know if there’s any need to go full Barolo on this one. You go Barbaresco, that’s the move. You go Barbaresco from Piemonte, at least six years old.”

Caleb:

“Brilliant, brilliant.”

Kenny:

“There’s nothing wrong with that. Sounds delicious to me. When are you coming over? You bring the wine, I’ll bring the pork chops.”

JC:

“I got a question for you, Kenny. I got I got a wine question for you. So, in the in the fra diavolo, you got you got some spice in there. And my suspicion is yours is probably a little spicier than than most. Do I have that right?”

Kenny:

“Well, I’m allergic to a lot of spice, so I’ll tend to be a little bit less.”

JC:

“Got it, okay. I like it a little spicier, so I have difficulty pairing that. I’m not Italian, I’m Cuban, even though I’m obsessed with Italian wine and food, like a lot of normal people. So, I have issues with that. I’m thinking like an Amarone because you’ve got a little bit of residual sugar in there. Because I hate to go white wine with that.”

Kenny:

“With the fra diavolo, you wouldn’t go white wine, I don’t think.”

JC:

“I don’t think so either.”

Kenny:

“I mean you could, but I think red with that is actually better.”

JC:

Right, but like what red? That’s why I’m thinking Amarone because you’re getting a little bit of that residual sugar. An Amarone della Valpolicella for those who are not…”

Kenny:

“I think that’s probably the right call. Because it’s not too heavy, and it gives you the right the right amount of sweetness for that dish. Especially if you’re going to make it spicy, like if you’re going to make it arrabbiata style.”

JC:

“I know. The problem is that Amarone ain’t cheap, man. They get you.”

Kenny:

“Duh. You see what inflation’s doing these days?”

JC:

“I mean, even before that, it’s one of one of Italy’s most pricey wines. You got Amarone, Barolo, Brunello. Those are the big ones. All my favorites, unfortunately.”

Caleb:

“Express passengers. This show has been taken over by two amazing chefs and wine experts. And I’m just letting it happen because I love it, and that’s just the way things go. And we love food and wine here, and we love your analysis. Great picks on the wine, great recipe recommendation, Kenny. I think that’s going to be happening this weekend for me and my family, so we appreciate that, and we appreciate you guys. Thanks so much for joining the Investopedia Express on our 100th episode. We love your analysis. You’ve been such good friends to the site, such good friends to me, and I so appreciate you both.”

Kenny:

“It’s a pleasure. Thanks for having me. And listen, when you make the pork chops, cover them tight because it’s the steam that they bake in that gets them nice and soft and juicy and ready to eat.”

Caleb:

“Thank you for that tip. JC, you’re the man.”

JC:

“Dude, this is fantastic. Thanks, Kenny. Love it.”

Term of the Week: Preferred Shares

It’s terminology time. Time for us to get smart with the investing term we need to know this week. But since it’s our hundy, we’re going to make this one extra special. You all know that I’m a struggling wannabe emcee. I love the flows, and I love finance, and I can’t help but put them together into a cheesy little sandwich for you every week. I’m sorry about that, but I have finally found my people thanks to the power of social media. Dex McBean has entered my consciousness, and my consciousness just got a whole lot nicer. He’s a freestyle finance rapper, for real. Not like me. For real. And I had to invite him onto the show to spit some rhymes with our term of the week. Welcome to the Express, Dex.

Dex:

“Thanks, Caleb. Let’s just get into it, man. Congrats on a hundred episodes. This is an accomplishment indeed. Investopedia Express, bringing the people up to speed. Expert investor or novice, we got the knowledge that you need. It’s time for me, Dex McBean, to rap the term the week. This term is something that you might not often heard. It’s not common, I’m talking preferred stock shares. One difference is, preferred shares yield a higher dividend and greater claim on assets if the companies liquidating them. Adding… protection that you get for your investment, except in non-voting shares, so save all your suggestions. Preferred shareholders get more say in the direction, but dividends be steady, long as they solvent then you get them. But if… and payouts get skipped, preferred shares get arrears for the ones they missed. But it’s not hopeless, another caveat is this: cause they’re so stable they’re unlikely for a huge capital gain… Preferred shares are rated like bonds for the strength of their investment, though they don’t offer the same level of protection. Hope you enjoyed the lesson and learned a bit about the topic. Let us know what term to cover next week in the comments.”

Caleb:

“What? Dex McBean just blowing it out with preferred shares. Great stuff.”

Dex:”

“You got some bars for me, Caleb?”

Caleb:

“Oh, I got something for you, man. Let me get that beat. Oh, no, you didn’t. Oh, yes, you did. Listen up, parents. Listen up, kids. That’s Dex McBean laying out FinRaps, dropping mad tracks to take it all back to the rack like Sprewell on attack, like Dragon Stout and Jerk Chicken click clack go his flows. He’s getting financial, listen real close. Chopping up your pencils, how to money right. He’s all about that info. Say hey, say ho. He’s getting influential, follow his rhymes. He’s got that potential, Brooklyn’s finest. He’s got those credentials. We’re burning it all down right here. The Express is smoking right now and not because of me. It’s so good to have Dex McBean. What a great suggestion, man. Tell the folks about who you are, what you do, and where we can find you.”

Dex:

“Oh, man, my name is Dex McBean. You can find me on social media, Instagram @dex.mcbean. I’ve got a financial literacy album called Wealth coming out. We all live to hustle all financial literacy topics. Shout out to Caleb and Investopedia Express episodes. Hundred episodes, glad I could be a part of it.”

Caleb:

“So good to have you, man. And you just made my day and made the 100th episode so special. Folks, follow Dex McBean. Check his stuff out on Instagram, on the Twitter. He is dropping finlit rhymes like nobody’s business, and that’s our business. So, we love what you’re doing, Dex. We’re going to have you back on this show real soon. Thanks for being here.”

Dex:

“Appreciate you guys.”