Tesla (NASDAQ:TSLA) has long been the odd duckling of the Magnificent Seven, the group of seven high-performing tech companies that have dominated the S&P 500 over the past year and change.

Unlike the other six…

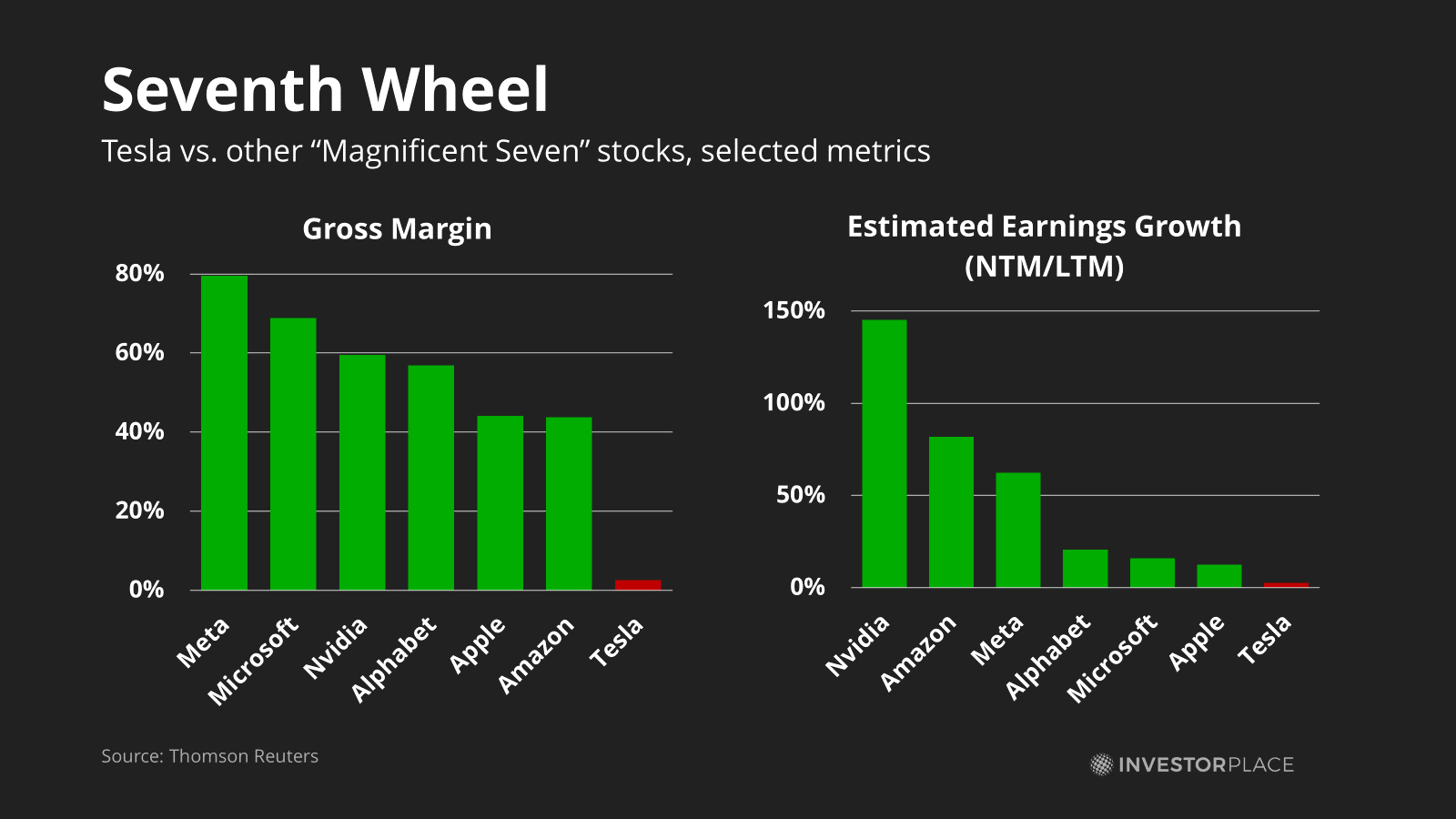

- Costs. Tesla makes its money from high-cost manufacturing, which depresses gross margins and lowers cash returns on investment. Auto manufacturing has never been – and likely will never be – “scalable” like software and other tech products.

- Competition. The firm is facing greater competition than the rest. Last month, China’s BYD (OTCMKTS:BYDDY) overtook Tesla as the world’s largest electric vehicle maker.

- Innovation. And its CEO’s top innovations are often siphoned into separate entities like Neuralink (brain implants) and Starlink (worldwide internet coverage). Tesla’s only revenue stream beyond EVs is in solar power.

Together, that makes Tesla’s balance sheet look more like an industrial firm’s than a monopolistic tech giant. By focusing his company on high-cost production, Elon Musk has left Tesla looking more like a regular automaker than the world’s next disruptor.

{kind=link}

That’s caused some problems for Tesla’s stock. Since January, its market capitalization has shrunk by a quarter. Most recent estimates peg U.S. EV growth at just 19% in 2024, down from a 45% jump the previous year, while potential competition from China could spoil the market further. Analysts believe Tesla will see its revenues rise just 14% this year, its slowest pace on record.

But what company could replace Tesla in the Magnificent Seven? Few firms have the same monopolistic bargaining power as the other six: Apple (NASDAQ:AAPL), Microsoft (NASDAQ:MSFT), Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL), Amazon (NASDAQ:AMZN), Nvidia (NASDAQ:NVDA), and Meta Platforms (NASDAQ:META). And even fewer have the raw financial resources to catch up or build their own “moats” in the tech industry.

Nevertheless, the writers and analysts at InvestorPlace.com – our free investment news site – have several ideas of which firms could replace the EV company. Even though Tesla still commands an outstanding A+ grade in my AI stock-grading system, MarketMasterAI, several pure-play tech firms could soon steal its place.

5 Stocks to Replace Tesla: Advanced Micro Devices (AMD)

In December, chip designer Advanced Micro Devices (NASDAQ:AMD) launched the MI300, a 3D “superchip” designed to take on Nvidia’s top AI products.

The design is groundbreaking. The new chip is roughly 30% faster than Nvidia’s top-of-the-line H100 design. And orders are already streaming in. AMD’s management estimates that sales will top $3.5 billion in the first year. That vaults AMD back into competition with Nvidia, a firm that currently ships 86% of the world’s AI accelerator chips.

It’s why InvestorPlace.com’s Tyrik Torres believes that AMD could become the “Next Big Thing for Chip Investors in 2024”:

The Instinct MI300X accelerator and the Instinct M1300A accelerated processing unit… work to train large-language models, and AMD CEO Lisa Su said these chips are comparable to Nvidia’s H100 but are “better on the inferenc[ing].”

All of this means, while AMD shares have risen more than 136% over the past 12 months, there is still enough upside potential to get new investors interested.

Of course, not everyone agrees. This week, David Moadel warns that optimism over AMD stock could be getting out of hand:

If you’re a contrarian investor, you may bristle at the ultra-optimistic consensus associated with AMD. You’ll bristle even harder when you discover that AMD’s GAAP-measured trailing 12-month price-to-earnings ratio is 1,353x. That not a misprint…

In other words, I don’t recommend pressing your luck with AMD stock at its currently stretched valuation.

AMD also faces an enormous uphill battle in AI acceleration software, an area that Nvidia has dominated for the past decade. Any software optimized for Nvidia’s CUDA platform needs to be rewritten for AMD’s open-sourced ROCm system.

Still, AMD is an attractive alternative for cloud computing firms seeking to reduce their reliance on Nvidia. And given AMD’s recent successes against Intel (NASDAQ:INTC) in the X86 server business, don’t be surprised if this underdog soon gives Nvidia a run for its money.

2. Broadcom (AVGO)

Shares of networking giant Broadcom (NASDAQ:AVGO) came within striking distance of Tesla’s market capitalization last week. The $20 billion difference was almost a rounding error for the $560 billion firm.

Broadcom is the most likely company to eclipse Tesla’s value in the coming months. The high-value chip and software business is a provenly strong aggregator of firms, and AI has recently turbocharged its networking business. Analysts expect net income to grow double-digits this year, outpacing Tesla’s growth fourfold.

That’s because demand for networking and wireless chips has been insatiable. Vendors from Cisco (NASDAQ:CSCO) to Arista Networks (NASDAQ:ANET) have seen revenues for networking chips rise double digits in the past quarter, offsetting far slower growth in other areas. Charles Munyi at InvestorPlace.com notes that Broadcom is an “AI beneficiary [that] increased its dividend by 14% and will see significant free cash flow growth”. Paul La Monica adds that Broadcom is one of five mega-cap stocks that could turn the Magnificent Seven into the ”Dynamic Dozen.”

Of course, several issues stand in Broadcom’s way.

The most obvious is that Broadcom focuses on high-tech enterprise sales, which is a historically cyclical business. Sales are expected to slow to single digits in 2026 as growth ebbs.

Broadcom’s M&A strategy also faces headwinds. The semiconductor industry now trades at enormous premiums, which largely eliminates Broadcom’s historical ability to cheaply buy up smaller companies and wring out efficiencies.

Still, investors might not care in the end. “Sorry, Tesla and Elon fans,” La Monica writes. “It looks like investors are finding other large-cap stocks to embrace so far in 2024.”

3. Eli Lilly (LLY)

In November 2023, the U.S. Food and Drug Administration approved Eli Lilly’s (NYSE:LLY) Zepbound, the company’s response to Novo Nordisk’s (NYSE:NVO) Ozempic and Wegovy weight-loss drugs. Studies found that Lilly’s entry was more effective at treating patients on average, with a regular dose helping people lose 25% of their weight.

Much of this news had already been anticipated. An earlier version of Eli Lilly’s weight-loss treatment, Mounjaro, had already been approved in 2022, and the company’s shares had already risen two-thirds in the year leading up to Zepbound’s approval.

But more upside is likely on the way. Today, roughly a third of Americans are overweight, and 36% are obese, according to the Harvard School of Public Health. These figures have more than doubled since 1980, driven by worsening diets and a spike in childhood obesity. Zepbound’s efficacy has also taken the medical world by storm.

That’s made Wall Street particularly bullish about Eli Lilly’s prospects. Analysts at Morningstar believe that drugs combating weight will generate $120 billion in revenues annually by 2031, split evenly between Novo Nordisk and Eli Lilly.

The figure could be even higher. While the federal Centers for Medicare & Medicaid Services currently does not cover weight-loss medications, lobbying to get these drugs approved for coverage from the American Medical Association has been intense. The benefits of weight-loss drugs also extend to diabetes, heart disease, and other risk factors that will be difficult for CMS to argue away.

It’s why Alex Sirois highlights Eli Lilly this week at InvestorPlace.com for its “strong buy” rating on Wall Street. Chris Markoch went a step further in January, calling Eli Lilly a firm with “massive upside”:

The real upside for Eli Lilly comes from projected earnings. In the next 12 months, the company expects to see earnings grow by 89%. Much of this is due to the success of its GLP-1 weight loss drugs Mounjaro and Zepbound.

Still, investors will want to tread carefully. Eli Lilly trades at a significant premium to its fundamental value of roughly $450, so it will need to achieve multiple years of super-normal growth to justify its current $660 price tag.

4. Netflix (NFLX)

In 2022, Forbes writer Peter Cohan proclaimed that “FAANG Is Dead.” Shares of Netflix (NASDAQ:NFLX), the “N” in that group, had fallen 70%, and few believed that the streaming giant could beat better-funded rivals like Disney (NYSE:DIS) or Amazon. The latter would splash out $715 million to launch The Lord of the Rings: The Rings of Power streaming TV series later that year.

But it turns out it’s harder to beat Netflix than it might seem. Amazon’s Rings of Power proved to be a flop; only 37% of people who started the series finished it, according to a study by Forbes. And even Disney has struggled to maintain momentum. In its most recent quarter, the media giant revealed that domestic paid subscribers to its Disney+ streaming service had increased by only 1% quarter-over-quarter. Disney-owned Hulu lost 100,000 online subscribers.

Meanwhile, Netflix has continued to push ahead. On Jan. 26, the firm revealed that subscribers had increased 5.3% quarter-over-quarter and 12.7% year-over-year. Margins have also expanded, rising from 7% to 16.9% in a year. Netflix now has roughly as many viewers as Prime Video and Disney/Hulu combined.

It’s why Netflix tops Joel Baglole’s list at InvestorPlace.com of “3 Hypergrowth Stocks to Buy and Hold Forever.” In an update this week, Baglole notes how Netflix is not only reasserting itself as the world’s dominant streaming company, but also the only profitable one:

As of yesterday, NFLX stock is up 12% after another strong earnings print. Growing subscription numbers are driving the share price higher. In the last six months, the stock has gained 30%, including an 18% rise so far in 2024. News that the company added 13.1 million net new subscribers in Q4 of 2023 has shifted the share price into overdrive.

Of course, an investment in Netflix comes with several risks. Firstly, subscriber growth will slow in 2024 as the benefits of cracking down on password sharing rolls off. Secondly, the firm is reaching saturation in the U.S. and Canadian markets, where roughly 55% of households already subscribe.

Finally, valuations are relatively stretched based on the financial resources Netflix must pour into content creation. A bottom-up valuation prices the streaming firm’s stock closer to $450, well below its current $565 market price.

Still, Netflix and most of the Magnificent Seven stocks have long shown that high-growth companies can often grow fast enough to fill in their valuations. With Disney and other competitors struggling, Netflix could take Tesla’s “Magnificent” crown.

5. Visa (V)

The final pick to become the next “Magnificent Seven” stock comes down to four stocks:

Each of these firms dominates its industry and has gross margins that exceed 70%. They’re also fast-growing, with earnings growth expected to top 15% this year. In other words, all look much like a Magnificent Seven stock.

Each also has its fans at InvestorPlace.com. Salesforce is favored by Michael Que for its GenAI-powered tools. Marc Guberti prefers Adobe for its relatively favorable valuations. And Luke Lango prefers Intuit for its strong AI tool set that is launching just in time for the 2024 tax year. (subscription required).

My favorite, however, is Visa, a company that has quietly become one of the fastest growing blue-chip stocks on the market. And here’s why I recommend it above all others.

In August 2023, my MarketMasterAI system began awarding Visa the top A+ score. And by December, the payments firm had risen into the Top 5.

A look under the hood quickly reveals the reason. MarketMasterAI uses analyst estimates (among other data points) to predict how markets will perform over the next six months. And these figures have been steadily rising for the past several months, especially among consumer-focused firms. Earnings-per-share estimates for 2024 at cruise firm Royal Caribbean Cruises Ltd. (NYSE:RCL), a bell-weather of U.S. consumer demand, have surged from $6 at the start of 2023 to $9.30 today. Airlines, home builders, and other cyclical firms are seeing similar upgrades.

That tells us that payment firms like Visa should perform marvelously over the next six months. Payment companies rely on rising spending, and we’re currently seeing a “goldilocks” environment of strong consumption and low default rates. Cross-border transactions are also returning on rising international travel. This is a particularly lucrative source of profits for firms like Visa and should keep margins high going into 2025.

Perhaps most importantly, Visa remains a monopolistic business that’s riding a secular wave of electronic payments. Its services are accepted almost universally, and its ubiquity in the financial system means it doesn’t matter whether consumers use credit, debit, or mobile for payments. As long as consumers are ditching cash, Visa will benefit.

That makes Visa stand out from the rest. It’s fast growing, lucrative, and able to maintain its leading position with virtually no effort. In other words, a perfect “Magnificent Seven” stock.

The Real Magnificent Seven

Fans of old Westerns will have doubtlessly watched the 1960 movie The Magnificent Seven, an adaptation of the 1954 Japanese epic Seven Samurai. In it, the ensemble cast, including Steve McQueen and James Coburn, join forces to defend a village against a gang of bandits.

[Mild spoiler alert] The fortunes of the seven vary wildly. Some survive the encounter, while others do not. The movie’s winding script, which leaned heavily on the Japanese original, is a masterclass on keeping viewers guessing.

This is probably not what Bank of America strategist Michael Hartnett thought when he coined the term “Magnificent Seven” to describe America’s top tech stocks at the time. To the uninitiated, the phrase sounds more like a “can’t lose” list of investments.

Life, however, often mimics art. Tesla’s 2030 bonds now trade at 82 cents on the dollar, depressed by fears of an EV slowdown. And analysts have cut their earnings per share estimates by 20% on average over the past 30 days.

That’s why Louis Navellier launches a new video this week that details how to navigate this new normal. In it, he reveals the Quantum Cash project, his newly upgraded AI-powered income system. Quantum Cash recently paid out a $3,375 windfall in a one-month time frame… $4,650 in three months… $11,925 in five months… and $16,875 in 11 months.

So, if you’re feeling a little behind in your retirement savings and want to build a second income stream (even if you have a smaller portfolio)… consider setting aside five minutes of your time to watch Louis’ critical broadcast, here.

On the date of publication, Thomas Yeung held a LONG position in shares in GOOG and GOOGL. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.